Saturday's sweeping storm toppled many a tree and flooded low lying areas during high tide, but the one thing the gusting 50 MPH storm didn't do was create damage that would necessitate the need for the type of storm shutters once finds in Hurricane alley beach-front bungalows. Yet, that's the requirement that homes within 3/4 miles of the Long Island Sound or portions of major rivers near the sound

Andover has about 2,000 customers in Connecticut who must add the shutters to keep their homeowner policies. The regulation applies to homes three-quarters of a mile or closer to a major river or Long Island Sound

State Rep Chris Perone, D-Norwalk, demanded an investigation "Shame on Andover, and shame on other companies petitioning to place such a financial burden on our shoreline residents, specifically those residents living in East Norwalk in close proximity to Long Island Sound. The financial burden of installing these storm shutters places economic hardship on shoreline residents battling the high cost of energy and those living on fixed incomes. This is unfair to the residents of Connecticut.”

House Speaker James Amann, D-Milford, and state Attorney General Richard Blumenthal called for the Insurance Commissioner Susan Cogswell to reverse the changes to coastal guidelines approved for Andover. Along with state Sen. Cathy Cook, R-Mystic, and state Rep. Ed Jutila, D-East Lyme.

Last Thursday, Blumenthal issued subpoenas to nine insurers. The subpoena requested each company to document their reasons for requiring the shutters. While Andover is the only company requiring the shutters, other companies indicate premiums will increase if the shutters are not installed. The companies subpoenaed Thursday are: Andover Companies; Main Street America Group Holdings; Met Property & Casualty Co., Vermont Mutual Insurance Group; New London Mutual Insurance Group Co.; Fireman's Fund Insurance Co.; The Allstate Corporation; Unitrin, Inc.; and Lumbermen's Casualty Company.

AP, Blumenthal questions insurers' mandate for shutters Friday September 01, 2006

The CourantStorm Over Hurricane Risks? August 25, 2006, By MARK PETERS

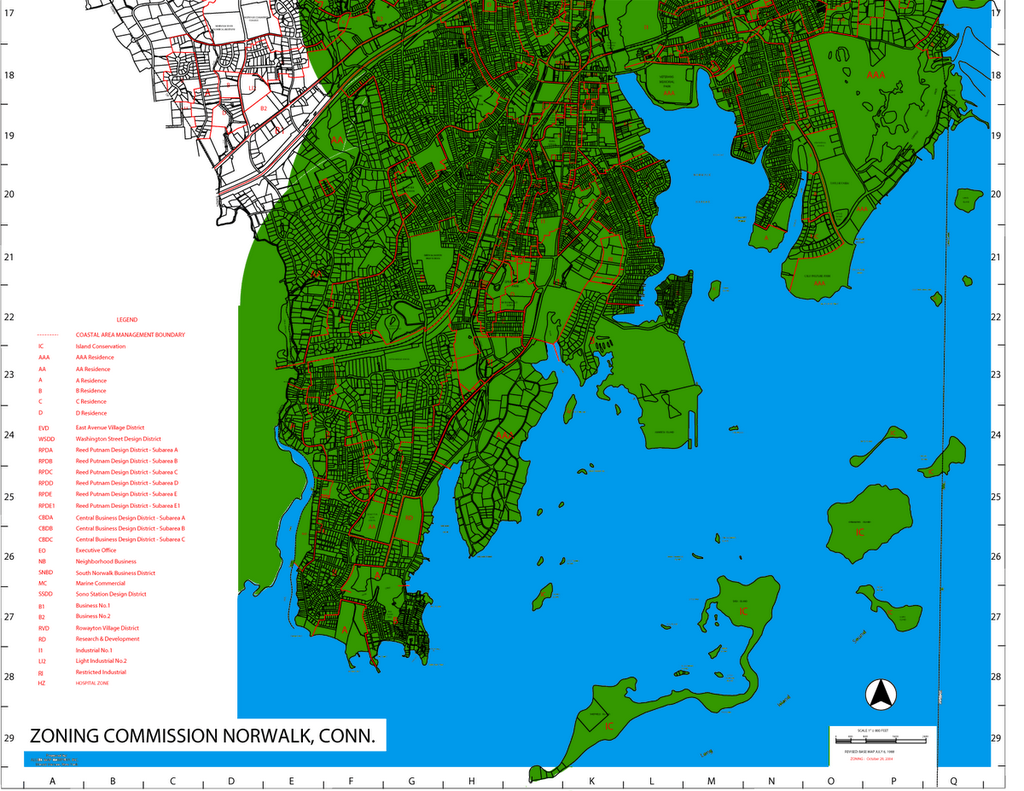

Updated: How this affects Norwalk, a map that shows half of Norwalk would have to install these storm shutters.

7 comments:

Well I guess people could that use Andover as their insurance carrier but who don't want or cannot afford shutters can always buy insurance from another provider.

If storm shutters really are not necessary, then there will be some insurance company out there that doesn't require them. Because the insurance companies certianly don't get kickbacks from storm shutter companies, so if they really don't matter, then they won't be required.

So why should people who live inland subsidize waterfront homeowners? I'm all for people living on the water, but they need to pay the extra insurance for the risk of storm surges and hurricanes. After all, they benefit from the view.

I just see no reason why people in Danbury need to subsidize waterfront homes in Greenwich or Stamford or Westport or anywhere else.

Why not price insurance commensurate with the risk involved? Why should certain people subsidize other people's riskier behavior?

Trees cause more storm damage than any other storm event, yet these same insurance companies are not proposing to increase premiums for all those homes that have large trees on the property.

It's very easy to determine if someone is within 3/4 of a mile of the shore, but it's very costly to determine if someone has large trees that could fall on the house. Especially since trees grow.

It's simply not cost effective for insurance companies to assess tree risks.

It's just not feasible for one company to come in and say we'll take this business, but not that. Once they weed out the higher risks, they have an unfair competitive advantage in dealing with the balance.

Say what? Insurance companies are in the business of assessing risk. Hopefully, they will be able to charge higher risk properties higher insurance, because otherwise the lower risk properties subsidize them. If you want to live on the waterfront or on a river, then you should have to pay more for flood insurance than a house that's on top of a hill. If you choose to have a burglar alarm, the insurance company will likely deem you a lesser risk, and charge less.

First off, we have one of the most vibrant insurance markets in the country, and the company in question is one of the smallest writers in CT...if people don't like Andover, they can go somewhere else. It's called competition.

Second, storm shutters are THE MOST cost effective way of reducing risk while keeping premiums and deductibles low. Most companies, not including Andover, are proposing either higher deductibles for wind OR installing shutters. The exhorbitant cost that Blumenthal has been citing ($100,000) is based on a single case for a multi-million dollar property in Noank, whose owners decided to go with remote-controlled shutters from a company out of Hyannis, MA. Not exactly baseline products.

Thirdly, inland policyholders SHOULD NOT have to subsidize coastal owners. Most companys, not including Andover, are talking about 1500 to 2500 feet from shore...not 3/4 mile. Most, if not all, of these properties are highly valued and owned by people who aren't exactly poverty-stricken. A family who owns a duplex in Hartford shouldn't have to pay more to ensure that Ned Lamont gets to keep his premium stable. Isn't this similar to the arguement liberals used to kill the Car Tax debate?

Why shouldn't a person who builds or buys a coastal home want to protect his/her asset from damage in a catastrohpic storm? Every insurance policy (auto, fire, life) requires that certain mitigation techniques be used for the policy to remain in force, ex. seat belts, defensive driving, dead bolts, smoke detectors, not smoking, etc. Statistics CLEARLY show that homes using storm shutters absorb far less damage in windstorms.

Also, the primary reason that homes lose their roofs in hurricances (and other high wind events) is that windows get blown out, pressure then builds up inside the house, causing tremendous upwards thrust on the roof. Combined with the drag created by the high winds coming up and over the roof, the roof is lifted, more wind is caught underneath, and the roof blows off--which not only damages or destroys the structure, but also ruins all the contents. Most HO policies have limited contents coverage, so even when the policy is honored, the homeowner is still left holding the bag on some of it.

All homeowners have numerous risk exposures, and it is up to each of us to identify those risks and decide on the best way to deal with them. In most cases, transferrance by way of insurance is the best way to deal with most. But we also have a duty to take appropriate steps to reduce the size and frequency of future losses. In some instances we decide to retain some risk ourselves (higher deductibles, self-insurance).

Final Question, why do you take such care to make sure that you clear ice and snow from your front walk and side walks? Answer: you don't want someone to slip and sue you. Your HO policy does provide liability coverage, but you have a duty to reduce the likelihood of such accidents. In the same vein, if there is a way to reduce the chance and size of a catastrophic loss in a windstorm, then policyholders should be encouraged to do it. Reducing the size and frequency of losses helps all policyholders by keeping rates low.

Trueblue,

waterfront communities do not pay more for flood insurance. they do have to gain admission into the NFIP, based on their floodplain history. once that is done, homeowners can purchase flood insurance from FEMA.

Trueblue said:

This isn't right, and the government should step in. Our insurance pools should be made as large as possible, and if inland folks subsidize shoreline Nutmeggers a wee bit, -- so be it.

That is ridiculous! So the privledged, rich few who can afford to live on the shoreline should be able to force inland homeowners to pay for their risk! That's a pretty good scam! Get someone else to hand over to you free money! Let's get the government to help steal money from some citizens to give to others!

Give me a break! It's one company. No one is entitled to cheap insurance. No more so than you are entitled to a cheap meal at restaurant, or a cheap car at the dealership. No one is required to give you a cheap good or service. The insurance company is not a slave to Connecticut shoreline residents. They provide insurance because it is a profitable venture for them. Just as it is a profitable venture for anyone to get a job and get a paycheck every week. There's nothing wrong with making money and making lots of it. This a free country. Don't like Andover, DON'T DO BUSINESS WITH THEM! Now that's a novel idea!

Post a Comment